Student loan payment pause will not be extended, White House confirms

White House press secretary Jen Psaki confirmed that federal student loan borrowers will need to resume making payments in February. (iStock)

The federal student loan forbearance period will end as planned on Jan. 31, 2022, White House press secretary Jen Psaki confirmed at a press briefing last week. Starting in February, federal student loan borrowers will resume their monthly payments.

- White House press secretary Jen Psaki

While the Education Department is "still assessing the impact of the omicron variant," Psaki said that "a smooth transition back into repayment is a high priority for the administration."

With less than 50 days left in the student loan forbearance period, several progressive Democrats including Senate Majority Leader Chuck Schumer (D-N.Y.) are urging President Joe Biden to reconsider this decision.

Keep reading to learn more about the end of COVID-19-related student loan relief and how to prepare your finances for payments to resume. Also, consider your alternative debt repayment options like student loan refinancing. You can browse student loan refinance rates from real private lenders in the table below, and visit Credible to see your estimated interest rate for free without impacting your credit score.

BIDEN ADMINISTRATION ISSUES 'FINAL EXTENSION' OF STUDENT LOAN PAYMENT PAUSE

3 ways to prepare for the end of student loan forbearance

A recent survey from the Student Debt Crisis Center found that 89% of fully employed student loan borrowers don't feel financially stable enough to resume payments in February. If you're part of this vast majority, here are a few things you can do now to prepare for the end of the federal student loan payment pause:

- Apply for extended forbearance. Federal borrowers may be eligible for up to 36 months of additional student loan forbearance by filling out a request for economic hardship or unemployment deferment.

- Enroll in an income-driven repayment plan (IDR). An IDR plan limits your monthly loan payment to 10-20% of your discretionary income, depending on the type of federal loans you have. You can sign up for this student loan repayment plan on the Federal Student Aid (FSA) website.

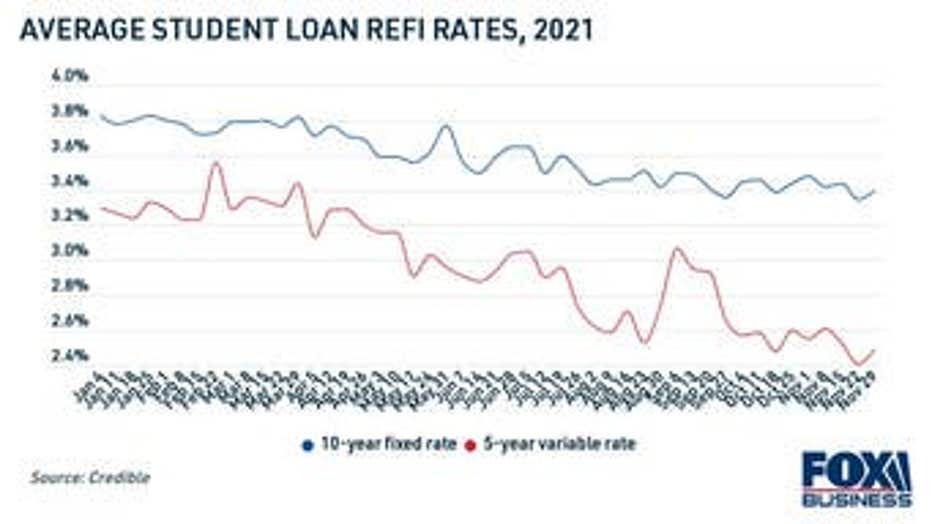

- Lower your monthly payments by refinancing. With student loan refinancing rates near all-time lows, there's never been a better time to lock in a lower rate on your student debt. Refinancing to a lower rate may help you reduce your monthly payments and avoid going into default.

Data showed that student loan borrowers who refinanced using Credible were able to save more than $250 on their monthly payments, all without adding to the total cost of interest over the life of the loan. To decide if refinancing is right for you, visit Credible to see your estimated rate with a soft credit pull. Then, use a student loan refinance calculator to determine your potential savings.

'BROAD' STUDENT LOAN FORGIVENESS STILL ON THE TABLE, EDUCATION SECRETARY MIGUEL CARDONA SAYS

Should you refinance your student loans?

Student loan refinancing can help you reduce your monthly payments and pay off debt faster. And since interest rates are near historic lows, now is the ideal time to lock in better terms on your student loan debt.

That being said, student loan refinancing may not be right for everyone. It's important to note that refinancing your federal loans into a private student loan would make you ineligible for government benefits like IDR plans, COVID-19 administrative forbearance and select student loan forgiveness programs.

You can also consider refinancing your private student loan debt since these loans don't offer the same federal protections. And if you don't plan on utilizing the benefits of federal loans, then the lower rates offered by private student loan refinancing may be worth the sacrifice.

Visit Credible to learn more about student loan refinancing from an experienced loan officer who can help you determine if this option is right for you.

PUBLIC SERVICE LOAN FORGIVENESS JUST GOT EASIER FOR 550,000 BORROWERS

Have a finance-related question, but don't know who to ask? Email The Credible Money Expert at moneyexpert@credible.com and your question might be answered by Credible in our Money Expert column.